The MFG-STK amount (from the Part Transaction History Tracker) divided by the number of units

Minus actual cost for one unit

The difference of these two lines is then multiplied by the number of units

And that product is what is we see in the usage variance.

For example:

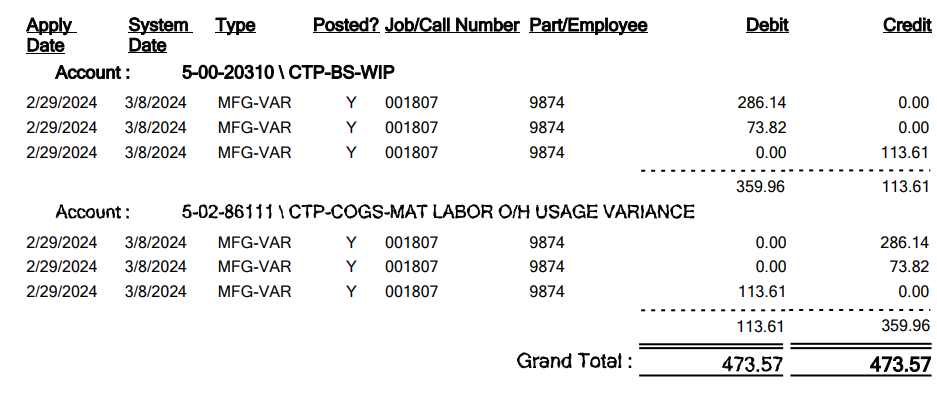

Order #: 1807

The MFG-STK for one unit is:

Date

Type

Quantity

Job

Invty

Amount

Mtl Unit Cost

Lbr Unit Cost

Bur Unit Cost

Sub Unit Cost

2/26/2024 12:00:00 AM

MFG-STK

2

1807

TRUE

2142.26

801.1622

55.365

214.605

0

Minus actual cost for one unit is:

Quantity

Job

Amount

Mtl Unit Cost

Lbr Unit Cost

Bur Unit Cost

Actual cost of Job for 1 qty :

857.97

18.46

71.54

The difference of these two lines is then multiplied by the number of units:

MFG-STK Mtl Unit Cost

Lbr Unit Cost

Bur Unit Cost

Sub Unit Cost

801.1622

55.365

214.605

0

Actual cost -857.97 -18.46 -71.54 0

56.80 -36.91 -143.07 0

Number of units x 2 x 2 x2 x2

Total: 113.61 -73.82 -286.14 0

This amt. is posted in

the usage variance account.

My question is why is the MFG-STK amount used to calculate the usage variance balance? Is there a reason why the MFG-STK is used and not the estimated amount found in the Production Detail report?

The variance from what I have found is what is left in wip when the job is completed.

All material, labor, burden minus MFG-STK,NFG-CUS material, labor, burden anything left or added after the last MFG-STK,MFG-CUS is the variance.

Lots of our people thought job closing was the magical moment, but the last quantity issued to stock is the point in time we have found.

So the theory would be similar. Estimates are a benchmark, but have nothing to do with costing.

Actual costs on job then the MFG-STK puts the item on hand at standard. Any differences or late issues will be put to the variance account.

Because when the parts are moved from WIP to Inventory they have to have a cost associated with them. The WIP value of the part is whatever costs have accumulated during the manufacturing process, but the Inventory value is determined by the Cost Method. If the part is Standard costed, the difference between the WIP value and the Standard Cost is the variance.

Inventory values are NOT updated if additional costs are added to the job AFTER the MFG-STK transaction.

I have this BAQ which gives an estimation of what variance could be. Of course the only way to know for certain is to run the Inventory/WIP Reconciliation report.