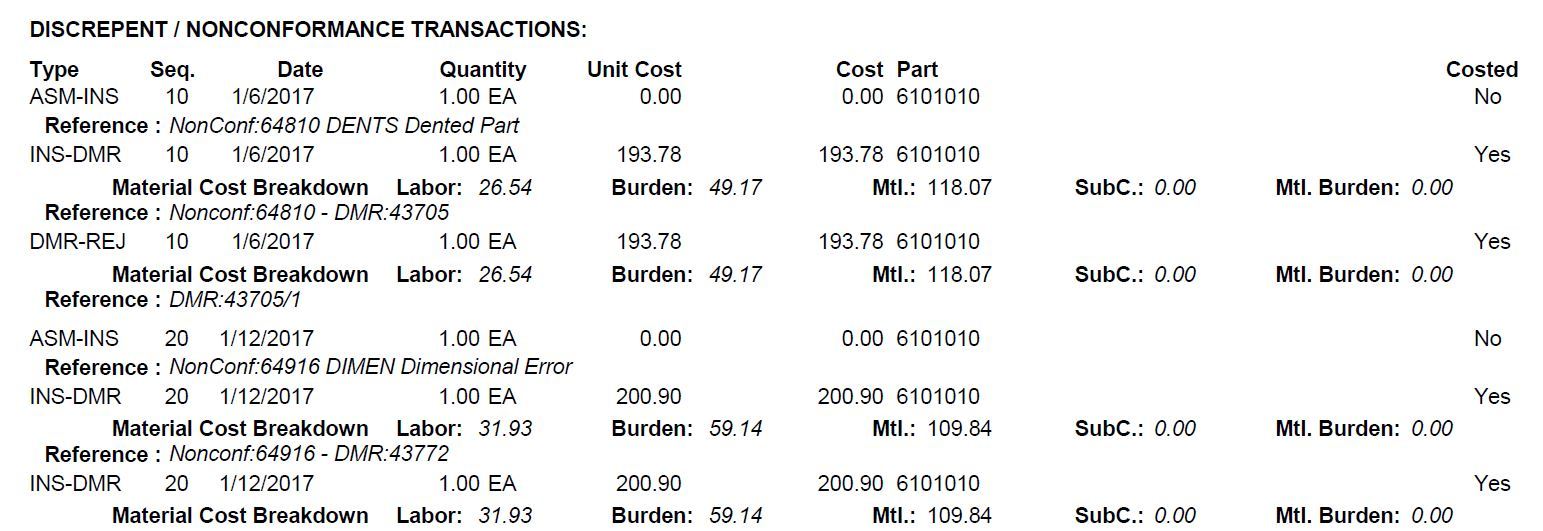

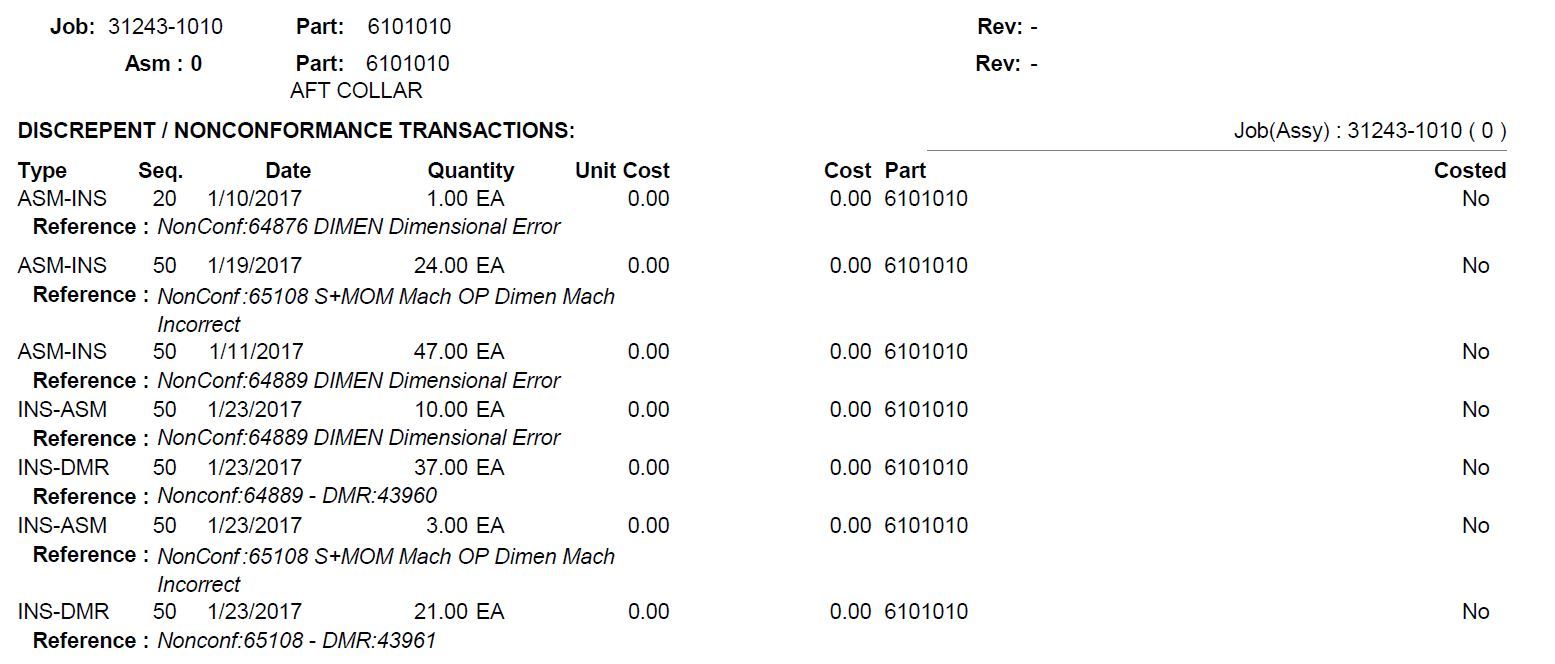

I have been wondering for awhile why some DMR’s are “costed” and others are not. Please see the attached pictures for an example. The “INS-DMR” and “DMR-REJ” transactions on page 1 (for small quantities of parts) are all “costed” – i.e., a value has been assigned to the scrap parts by Epicor. However, the “INS-DMR” transactions on page two (for large quantities of parts) are not costed. It’s the same part number on the same job, but it’s not being treated consistently.

I have been assured repeatedly by the people who input the DMR transactions that there is no “check box” or anything that they are aware of in the input screens which would cause some transactions to be costed and others not.

In this particular case, the uncosted DMRs probably represent expense of at least $12,000!!! This is quite a bit of expense that is not being recognized. The only difference that I can immediately see between the costed and uncosted transactions is that they are on different job operations. Don’t see how that would affect anything, though.

Any help would be appreciated as we are pulling our hair out on this one…We are on an “average” cost system if that matters.

Actually, a DMR, even a REJ, shouldn’t be costed if it’s from a job. From inventory, that would have to be adjusted from inventory, but from a job, the cost will remain on the job regardless and be spread somehow over the costs of the parts or put into variance for the job, so no accounting should take place from an Opr DMR.

Actually, if your parts (being produced on the job) are Average or Last cost based:

Labor non-conformance source DMRs pull the estimated costs (up to the offending OP) of material & labor & subcontract OP into the DMR. The asset value of what is received from the job is reduced by that amount if the DMR is rejected (and depending upon your GL controls, determine where that DMR rejection cost goes in the GL).

It works very well if you also are set up to adjust job yield (qty) to reported losses. (Without the yield process, you end up with additional job completion/closing exceptions & WIP variances when WIP is cleared.)

Job material non-conformances are similar (but simpler) - cost of the material is pulled into the DMR as a reference & removed from the job to reduce the unit cost of the receipted qty’s.

Timing plays a role. (Wait too long and/or don’t yield adjust job qty’s and you can get odd results.)

I imagine Std basis parts being produced on a job would always hit inventory on receipt as that std unit cost & the DMR would simply be a vehicle to capture some of the variance (from standard) cost.

Our sold items (jobs linked to sales order line releases) are all standard & appear to behave this way (although it never hits inventory… It goes against Cost of Sales account.)