Our drawings are considered master, and we use that BOM to import the materials for a given revision’s materials (part number and quantity).

To ensure consistency between our drawing and the job traveler, we’d like to include the expensed items (for example, bolts and o-rings) in a job’s materials, including the required quantity.

Supposedly this isn’t possible, but I find it a bit hard to believe that all manufacturing companies set all bolts, o-rings, etc. as stocked and quantity bearing.

Does anybody have experience with this situation? If so, what was your solution?

Yes set them as Non Qty bearing parts and add them to the BOM. I have many customers that add not only expense/MRO items but a few actually create specs and CNC programs that are NonQty bearing part number reference docs that can also be added to a Job Bom.

Its not as much as an issue with having non-qty bearing parts on a BOM, as it is how to cost them.

When you say they are expensed items, i assume that means they hit an expense account when received against the PO. When they are used in production do you want their cost to be part of the COS, with any use in production being a credit (or ist it debit?) To the expense account?

Or are you okay with their cost solely being in tge expense account?

Edit-

Also, you can use a part number for a BOM material, even without it being in the part file. It would be purchase direct. When a job is created, that purch direct line would make a purchase suggestion of type Buy to Job. When the part is received, its cost goes directly to WIP, and will eventually be included in COS.

You sure can. No impact with variance at all because they are NonQty bearing there is no inventory transaction associated.

However… one minor exception. Usually expense/MRO items you buy on a PO and they expense as soon as the PO is received. The NonQty bearing items would only be a reference on the Job Traveler as to where they get used, but there is no cost impact to the job as the items were already expensed… So here is the exception, you can technically make a Purchase Direct PO for NonQty bearing parts on a job IF for some reason you wanted those parts as Direct cost. I have ZERO customers who do that. They all do the previous example of an Expense PO receipt with the NonQty bearing part on the job with Qty as refeence

We are fine having the cost being solely in the expense account and NOT wrapped into the COS. Since this is the case, we can receive the PO, have it hit an expense account, but still keep the items in a BOM with a quantity (again, assuming they are non-quantity bearing but still stocked items)

And I think I understand the exception, and don’t anticipate ever doing that.

As long as you don’t actually issue those “pre-expensed” parts to the job they’d never get into wip or COS.

You’d have to give it more thought if you backflush, or use STD costing.

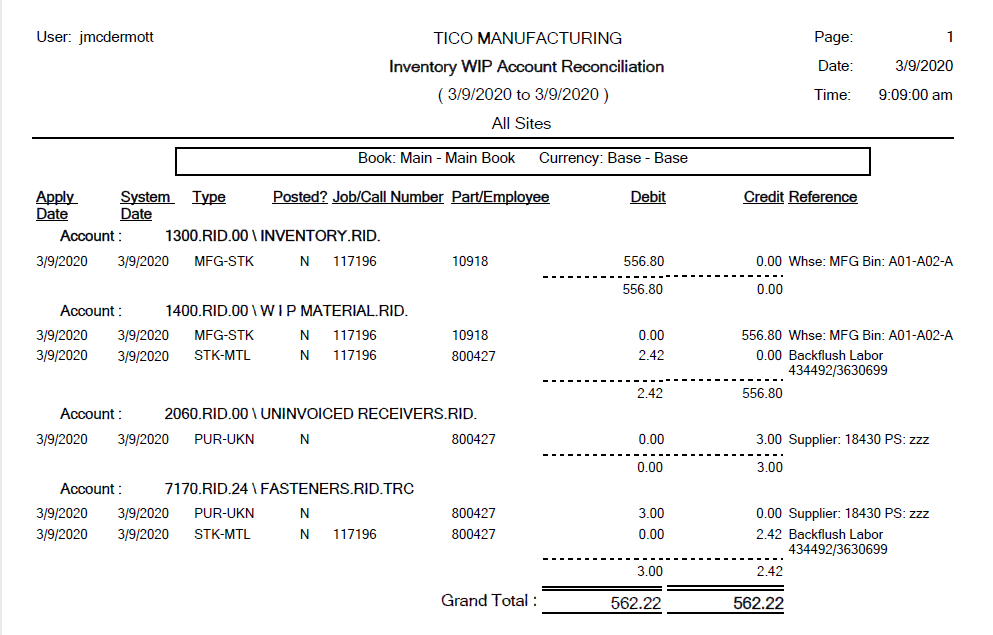

@JasonCampbell - There would be a variance if the parent part uses STD costing and is costed based on the BOM roll-up, which would include a cost for the expensed part. When all the materials are issued (except for the expensed part), there would be a difference. Thus a Variance generated.

I think the cleanest thing to do is

Make a Part Class for Pre-expensed parts, with a GLC pointing to the expense account (when it would normally point to the Inventory account).

Set these parts to that part class and enable qty bearing.

Use them on the BOMs like a normal part.

Make a Qty Adj Reason code for “Pre-expensed Adjustment”, with a GLC using the same acct as the expense account in the Part Class.

Typical flow would be like so:

PO Purchase of the part.

PO Receipt of said part debits the GL acct in the part class instead of Inventory. QOH is increased.

That part is issued to a job. This credits the GL acct used for the expense, and debits WIP.

The job is received into stock or shipped. The portion of the WIP for that part becomes COS.

Because this part isn’t inventory, and it’s QOH may not actually match the actual amount, a qty adj can be dine using the reason code created above. This will reduces the QOH, but cause no change to the GL (it would credit and debit the same account).

Exclude this part class when doing a Physical inventory or running Stock Status.

A good side affect of it being qty bearing, is that you’ll know if you have the parts to meet demand. As long as the Qty Adj is done regularly to make up for when the parts are used for non-system things (building maintenance, R&D, “government jobs”, etc…)

Agreed with everything said so far, but you all implement this far differently than we do.

Small nuts and bolts (etc.) are expense here. In setup, this means they are:

Non-qty-bearing

Go to an expense account (there are many here) via the part class GL code

Listed on the BOM (material on jobs eventually)

Backflushed or issued to the jobs

This means the cost goes to the jobs but the inventory quantity is always zero. It gives us (more) accurate job costing without managing the inventory.

Big disadvantage to me is that non-qty-bearing parts MUST be standard costed. Ugh. We wanted it to be last for expense parts. If we don’t even want to manage the inventory, why on earth would we want to micromanage the cost of items worth pennies?!

If costs are expensed (hitting the Income Statement once) and then are issued to a job (job-cost), are you not double expensing when that costs are later flushed from WIP upon close (hitting the Income Statement a second time)?

If the GLC’s are setup right the Expense Account will get debited (or is it credited? - whatever is the opposite of what happens when the Job is costed)

I’d be interested in seeing the T-accounts for the three transactions that makes that work. It’s REALLY important to get those GL Controls right though!

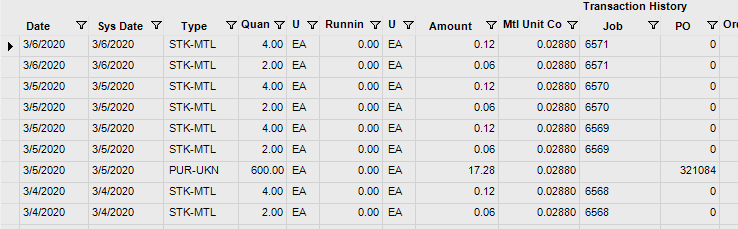

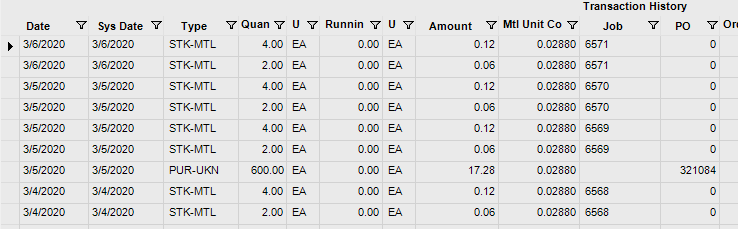

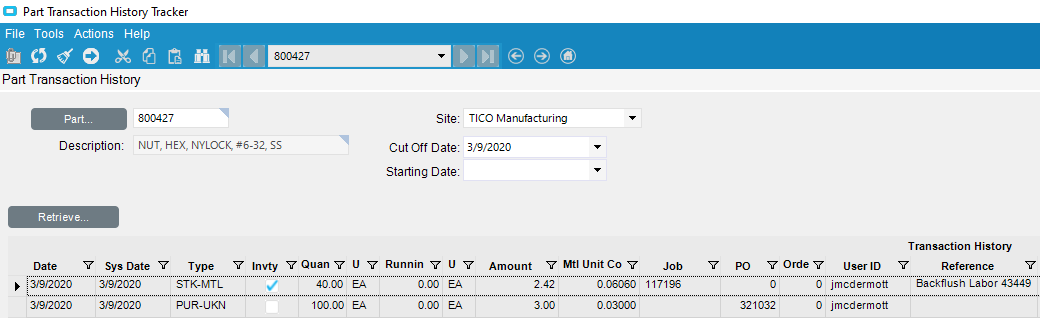

Im not sure if the STK-MTL happens for non-qty bearing parts.

We have some parts that are “mostly” shop supplies, but some times used on jobs or orders. We have them marked as Qty Bearing, but have a part class that uses an expense GL Acct, instead of the standard Inventory Acct. We exclude these from inventory counts.

Purchases are “to stock” (PUR-STK), and are “expensed” upon receipt, by the fact that the shop supplies expense is hit.

If we include a shop supplies part on an order (or job), a STK-CUS (or STK-MTL) tran happens, and the shop supplies account is credited.

So then the costs are not going to the job like Jason was saying? This is what raised my eyebrow. As I said, I’m an amateur accountant so I could be completely wrong. Of course the best way to prove these things is with a Pilot Database and a little time…